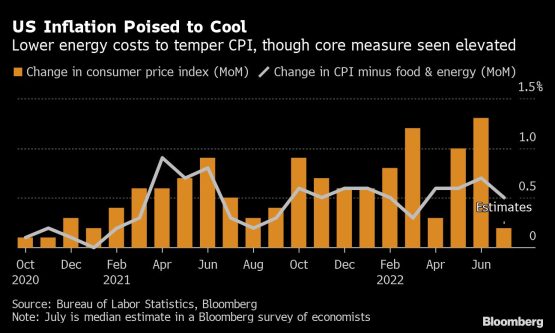

US consumers finally found some relief last month at gas pumps as fuel prices fell, though core inflation continued to simmer, economists project for data this coming week.

The closely watched consumer price index is seen rising 0.2% in July from a month earlier, which would be the smallest advance since the start of 2021. However, the so-called core measure, which strips out energy and food, probably climbed a concerning 0.5%, based on the median estimate in a Bloomberg survey of economists.

While moderation in the overall gauge is a welcome respite, the pace and breadth of inflationary pressures remains intense.

After a sizzling July payrolls report that included a larger-than-forecast pickup in hourly earnings, Federal Reserve policy makers remain tilted toward large interest-rate hikes.

Regional Fed presidents Charles Evans of Chicago and Neel Kashkari of Minnespolis are scheduled for separate speaking events. San Francisco Fed President Mary Daly will appear Thursday on Bloomberg Television, a day after the CPI figures.

The producer price index and University of Michigan consumer sentiment index will also be released this week.

What Bloomberg Economics says:

“The July jobs report settles it — we are not in a recession. More importantly, it also means the Fed will likely have to hike by another 75 basis points in September.”

– Anna Wong, Yelena Shulyatyeva, Andrew Husby and Eliza Winger, economists.

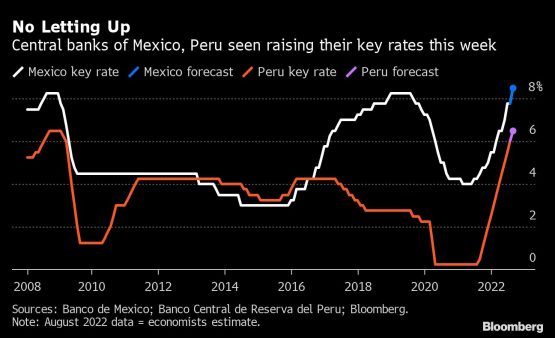

Elsewhere, the UK economy’s first quarterly contraction in more than a year, as well as mixed signs from Chinese price data, are likely to be among the highlights. Rate increases may materialize in countries including Mexico, Peru, Serbia and Thailand.

Asia

China’s trade data for July, released on Sunday, showed exports remained a rare bright spot for the world’s second-largest economy. Inflation statistics due mid-week are set to indicate continued moderation in factory-cost gains and a slight pickup in consumer-price growth.

South Korea’s jobless numbers are likely to reveal continued tightness in the country’s labor market, supporting quickening inflation.

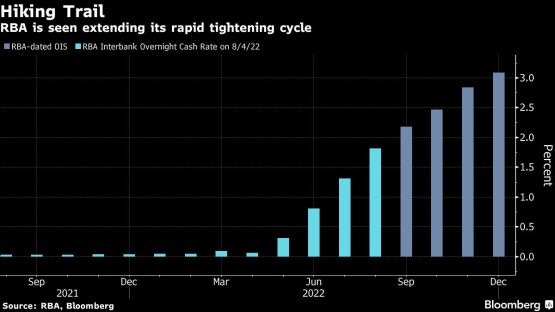

Down under, household spending and business conditions data will give clues as to how much Australia’s tightening cycle is weighing on the economy.

Producer prices data in Japan is set to show firms remaining under pressure from rising raw material costs, strengthening their case to pass those burdens on to consumers.

The Philippines announces GDP data on Tuesday, and Malaysia posts its national accounts numbers on Friday.

The region’s central bank highlight this week will be Thailand, which is anticipated by economists to raise its interest rates by a quarter point on Wednesday.

Europe, Middle East, Africa

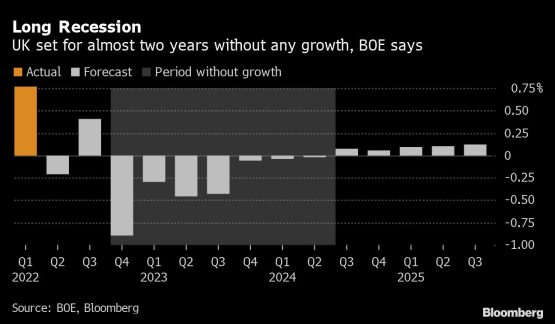

With the Bank of England having just warned that the UK faces more than a year of recession, evidence of an initial contraction might emerge on Friday.

GDP data will show a second-quarter drop of 0.2%, according to the central bank. While growth probably resumed during the current three-month period, a prolonged slump, reminiscent of the 1990s, will then likely ensue, its forecasts show.

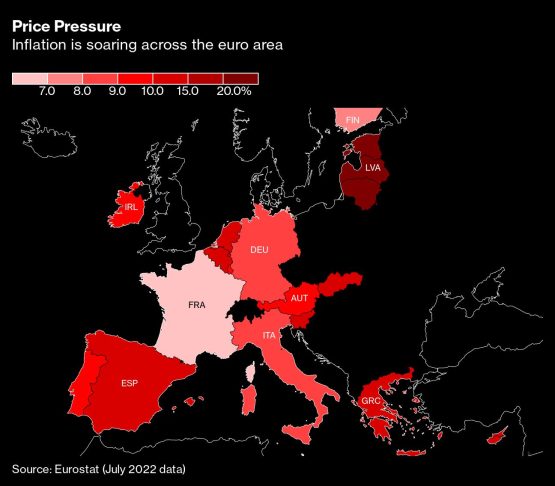

The same day over in the euro zone, the main data will be industrial production for June. While expected to gain for a third month, the report may also signal slowing momentum, with a median prediction to increase just 0.1%.

Investor attention will also be drawn to inflation data throughout Europe. Final data for the euro area’s four biggest economies will be published during the week.

First glimpses of inflation for July in Norway on Wednesday and Sweden on Friday will be of interest, with any acceleration likely to pile on pressure for more central-bank tightening.

Even faster price increase are taking effect in eastern Europe, with Hungarian data on Tuesday seen accelerating to 13%. On Wednesday, Ukraine will reveal its own rate of annual price growth, last reported at 21.5% for June.

By contrast, Russia’s inflation probably fell for a third month in July. Those data, also due Wednesday, will be closely watched for clues on the policy of the central bank, which cut its rate more than expected in June and said more reductions are possible.

Second-quarter GDP data due there on Friday may show an annual drop, and give an indication of the depth of the contraction since President Vladimir Putin started his war in Ukraine.

Europe’s only rate decision this week will be in Serbia, where the central bank might resume faster hiking.

In Turkey, current-account data on Thursday will likely show a widening deficit, although rising tourism and services revenue may mitigate some of that. And Egyptian statistics on Wednesday may reveal inflation accelerated further in July.

Two monetary decisions are due in Africa. On Thursday, Rwanda’s central bank will likely increase its rate for a second time this year, and Uganda is expected to follow suit on Friday.

Latin America

Inflation and the central-bank response take center stage in Latin America.

On the inflation front, Chile’s policy makers won’t have much to like about July’s report. Analysts see annual consumer-price increases of 13%, more than four times the target. Argentina’s July monthly reading may hit 7%, with the annual rate breaching 70%, the second-fastest in the G-20 after Turkey.

In Mexico, the move up in consumer prices will be much less pronounced but still come as unwelcome news to Banxico. Look for headline prints of over 8% with the core results not far behind, almost three times the central bank’s target.

By contrast, early estimates of Brazil’s July consumer price report see monthly deflation and the biggest year-on-year drop in nearly two decades. Inflation there may finally be on a long, slow glide back to target.

As to monetary policy, minutes of the Brazilian central bank’s Aug. 3 meeting, where policy makers raised the key rate to 13.75% and suggested they may not be quite finished, are due Tuesday.

On Thursday, analysts are all but unanimous that Banxico will hike for a 10th straight meeting, pushing the key rate to a record 8.5%. Peru also isn’t done with its record tightening cycle, likely keeping a sure-and-steady half-point pace to reach 6.5%.

© 2022 Bloomberg L.P.

For all the latest Business News Click Here

For the latest news and updates, follow us on Google News.

Denial of responsibility! NewsBit.us is an automatic aggregator around the global media. All the content are available free on Internet. We have just arranged it in one platform for educational purpose only. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, all materials to their authors. If you are the owner of the content and do not want us to publish your materials on our website, please contact us by email – [email protected]. The content will be deleted within 24 hours.