The rising cost of living is biting businesses and households around the world. Editors from across The Conversation’s international network have asked local academic experts to explain how their countries and regions are tackling this issue, as well as the 2023 outlook for prices and interest rates where they live.

This article is the third in our series on where the global economy is heading in 2023. It follows recent articles on inflation and energy.

UK: recession on the horizon

Alan Shipman, Senior Lecturer in Economics, The Open University

At first sight, the UK’s cost of living crisis might look fairly mild compared to other countries. Its inflation rate was 10.7% in November 2022, compared to 12.6% in Italy, 16.% in Poland and over 20% in Hungary and Estonia. But the Bank of England expects a recession in the UK this year – possibly lasting until mid-2024.

This is because the proportion of UK households that lack insulation against financial setbacks is unusually large for a wealthy economy. One pre-pandemic survey found that 3 million people in the UK would fall into poverty if they missed one pay cheque, with the country’s high housing costs being a key source of vulnerability. Another recently suggested that one-third of UK adults would struggle if their costs rose by just £20 a month.

The pandemic saw over 4 million households take on extra debt with almost as many falling behind on repaying it. And recent jumps in energy and food bills will push many over the edge, especially if heating costs remain high when the present government cap on energy prices ends in April.

UK governments have been stealthily raising taxes since 2010 and in real terms (adjusting for inflation) typical UK household income was already 2% lower in 2018 than in 2007. But real incomes have been further eroded over the past year since the UK’s 10.7% inflation rate (as of November) is far above the pay increases many employees have had to settle for in recent months.

But recent events have forced the government to make decisions that were not necessarily aligned with the looming recession. In September 2022, Liz Truss became prime minister with bold pledges to cure the UK’s economic malaise. The global financial markets responded dramatically to her tax cutting plans by hiking the interest they charge the UK government and businesses to borrow. This forced the newly installed chancellor Jeremy Hunt to embark on another round of public spending cuts and tax increases in November – actions governments usually reserve for the height of a boom, not the eve of a slump.

aslysun / Shutterstock

The Bank of England is also doing the opposite of what central banks prefer to do before a downturn. High inflation forced it to raise rates to 3.5% in December, with more rises expected in 2023. This boosts debt repayments for the millions who’ve borrowed to buy their homes, not to mention those with unsecured credit card or overdraft debt.

All of these additional costs subtract from a household’s disposable income. And because household consumption makes up close to 60% of all spending in the UK economy, this will inevitably lead to recession – which could well turn out to be very painful and very long.

US: central bank signals caution

John W. Diamond, Director of the Center for Public Finance at the Baker Institute, Rice University

Inflation increased significantly in the US in late 2021 and early 2022, reaching levels higher than at any time in the last 40 years. The Federal Reserve responded by aggressively raising its benchmark rate (the federal funds rate) seven times since March in an effort to stabilise prices. A couple of smaller increases are expected in 2023.

The US consumer price index, a standard measure of inflation, shows that prices peaked in June 2022, increasing by 9.1% over the previous year. The index has decreased every month since June, with the November data – the most recent available – indicating that US prices are 7.1% over the prior 12 months.

The fed funds rate serves as a benchmark for other interest rates, such as mortgage rates. Its recent increases have started to reduce demand for goods and services and investment. For example, existing home sales in November were 7.7% lower than in October and are down over a third from a year earlier. The underlying reason is that mortgage interest rates have more than doubled to over 6%, after reaching 7% in October, from 3% in the beginning of 2021.

The ripple effects of the reduction in housing demand will continue to slow economic activity for months to come because some of the impacts of monetary policy occur with a lag.

Juice Flair / Shutterstock

The Fed is now signalling that it will continue to raise interest rates in early 2023 before pausing, a cautious approach that is justified by a variety of economic data. This is partly due to continued strength in the labour market as unemployment remains low, wages that haven’t been adjusted for inflation continuing to rise, and roughly 10 million jobs remaining open, according to the latest data. To the extent that companies have to raise wages to attract or keep workers, this may lead to higher prices and persistent inflation.

This issue is especially important given the ageing population in the US and the effect it has on the labour market. At the same time, the recent fall in energy prices is unlikely to continue, so further reductions in inflation will have to come from declines in other areas, such as shelter and food.

Australia and New Zealand: using restraint to ease inflation

Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

The regular survey of economic forecasts published by The Conversation Australia at the start of 2022 was titled: Top economists expect RBA to hold rates low in 2022 as real wages fall.

This forecast for how the Reserve Bank of Australia would set rates in 2022 was spectacularly wrong. The second part turned out to be pretty right: real wages did fall, although not because they continued to barely grow as the experts had been expecting, but because their growth was dwarfed by an explosion in inflation.

After hovering below the Reserve Bank’s 2-3% target band for most of the previous five years, Australia’s annual rate of inflation began 2022 at 3.5% but shot up to 5.1% in March after Russia invaded Ukraine and reached 7.3% for the year to September. The bank expects something close to 8% for the year to December when the figures are next updated in late January.

Australia’s neighbour New Zealand has experienced much the same thing, with an inflation rate that also hit 7.3% and has since slipped to 7.2%. But its response has been dramatically different.

Whereas Australia’s Reserve Bank increased its rate in eight small monthly steps from May, either by 0.25 or 0.5 points, New Zealand’s Reserve Bank began pushing up rates much earlier and more aggressively – including a recent 0.75 point hike, even as it forecasts a New Zealand recession.

In Australia – unlike New Zealand, the US, the UK and much of the rest of the developed world – a recession isn’t commonly forecast, largely because of the bank’s restraint in the face of a three-decade inflation high. This approach has served Australia well over the 29 years until the COVID recession in 2020. The country avoided the “Great Recession” after the 2007-08 global financial crisis and the 2001 “tech wreck” recession that hit the US and much of the rest of the world in 2001.

This restraint also reflects a belief among authorities that a wage-price spiral isn’t taking hold in Australia. Wage growth remains mired at 3.1%, well below New Zealand’s 7.4%.

And inflationary pressure seems to be easing. Global oil and wheat prices are down one-quarter to one-third from mid-2022 peaks following Russia’s Ukraine invasion. The Reserve Bank reckons Australian inflation will slide throughout 2023, slipping to 4.7% by the end of 2023, and to 3.2% by the end of 2024, almost back to its 2-3% target band.

By being less hawkish than its global counterparts, the bank hopes to remain on the right side of history.

France: managing price increases relatively well (for now)

Aymen Smondel, Maître de conférences en finance and Mohamad Hassan Shahrour, Maître de Conférences en Finance, Université Côte d’Azur, IAE Nice – Université Côte d’Azur

Inflation is an area where France appears to be more resilient than its neighbours. In December 2022, the country’s inflation rate (measured by the consumer price index) was 6.1%, compared with 10% in Germany, 11.8% in Italy and 9.3% in the UK.

The main challenge facing countries, and contributing to inflation – or even stagflation (which refers to a combination of inflation and low economic growth) in the case of some economies – is the huge increase in energy prices in recent years.

Faced with this rise, the total French state budget devoted to mitigating household energy bills is set to reach at least €75 billion (£66 billion) across 2022 to 2023, through schemes including energy vouchers and a tariff shield.

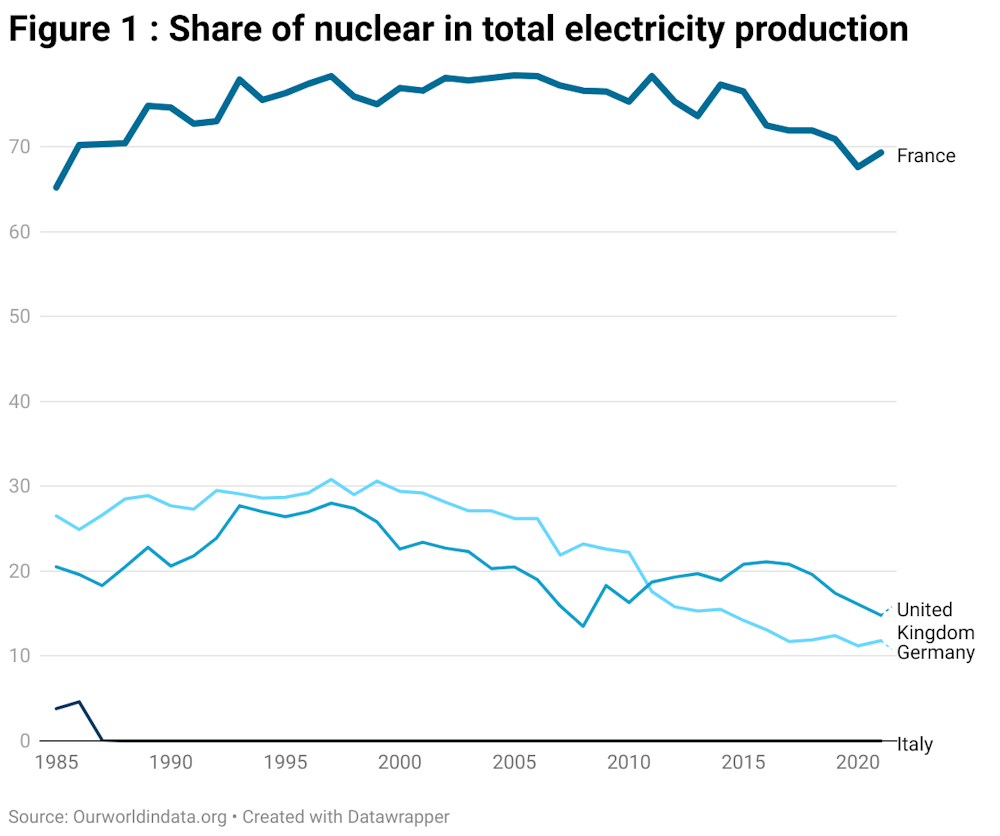

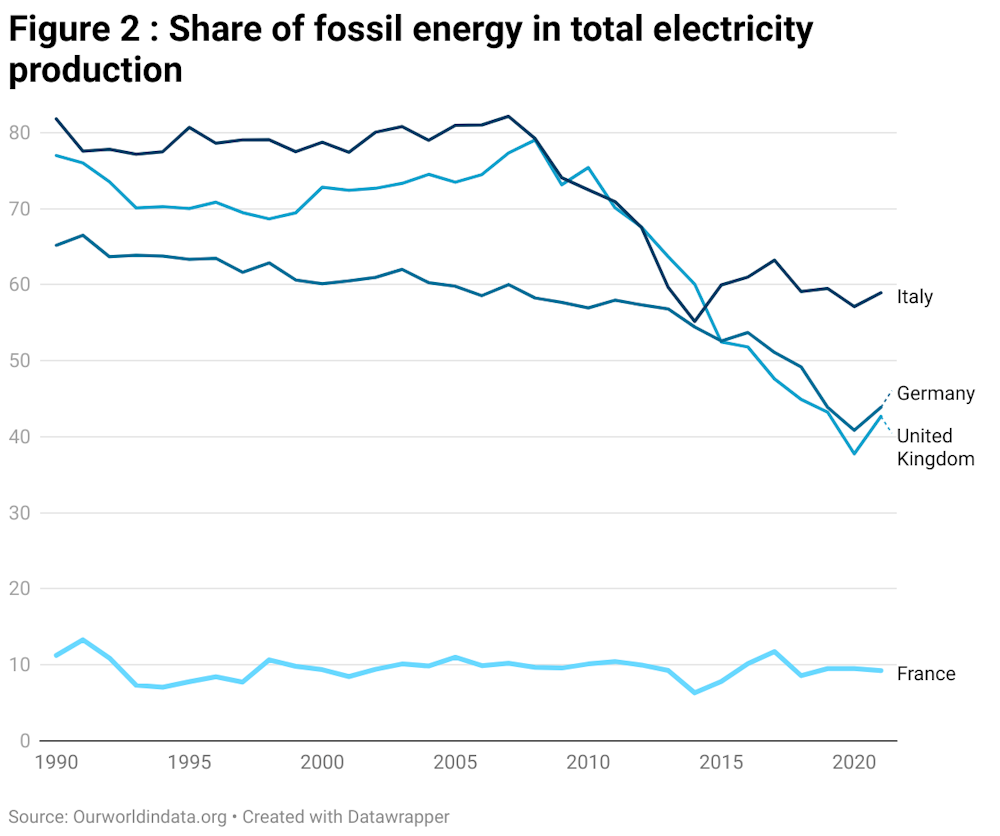

These actions have kept the inflation rate well below that of most European economies. In addition, France is less reliant on fossil fuel products, and therefore less vulnerable to energy price fluctuations.

While the chart above shows France’s use of domestic nuclear power sources, the chart below shows that other countries rely more on – often imported – fossil fuels.

Energy issues aside, countries are also impacted by the global market just like companies are affected by their institutional environment. As a result, future changes in public policy could influence the inflation rate, which may or may not have peaked.

For example, the European Central Bank’s decision to raise interest rates for the first time in a decade last July could weigh on countries’ budgets, giving governments less room for manoeuvre as they try to contain price increases.

Without some regional stability in terms of politics and economics, France may not be able to continue to outperform its neighbours in the coming months.

This is an edited excerpt from an article published in October 2022.

Spain: inflation, public spending, deficit and debt

Luis Garvía Vega, Director del Máster Universitario en Gestión de Riesgos Financieros (MUGRF) en ICADE Business School, Universidad Pontificia Comillas

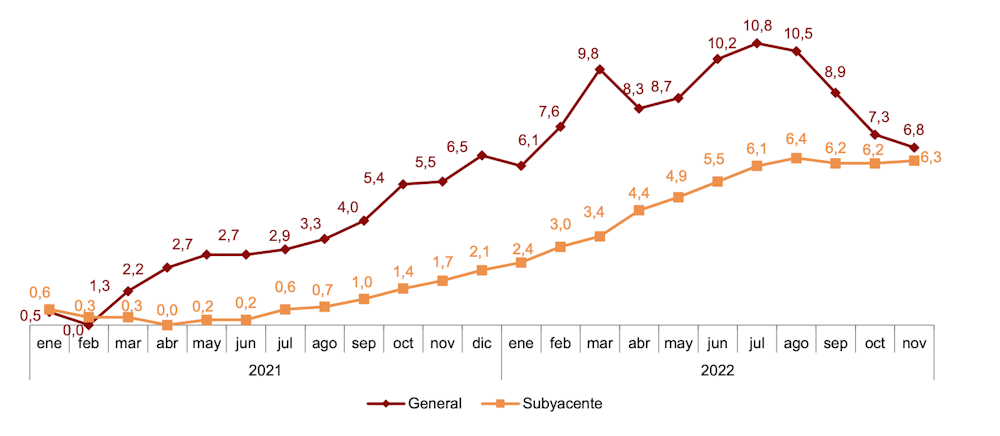

After beginning 2022 with inflation at 6.1%, Spain’s consumer price index peaked at 10.8% in July before closing out the year at a rate of 6.8%. Taking into account the 2021 inflation journey from 0.5% in January, to 2.9% in July and 6.5% in December, it now looks like price rises are being brought under control.

Core inflation (which excludes unprocessed food and energy) saw a more gradual but sustained rise. It was 2.4% in January 2022, peaked at 6.4% in August and fell to 6.3% in November. The closing gap with headline inflation during the final quarter of last year was mainly due to government measures to control the rise in energy prices.

Inflation in Spain, 2021-2022

National Statistics Institute (INE), Spain

Like many other countries, Spain lacks control and efficiency when it comes to public spending. The country’s pension system must support a rapidly growing older population; it is highly dependent on fossil fuels; the unemployment rate has been above 10% since 2008; and – again like other countries – it is suffering from deep political and social polarisation right now. A high public deficit has also helped inflate the Spanish debt bubble.

Sergii Figurnyi / Shutterstock

But this is an election year for municipal, regional and general government and so major reforms will be difficult – particularly anything that affects Spain’s 9 million pensioners or its more than 3 million public workers.

Digitalisation and training could provide a solution by supporting more efficient management of resources. This could help to gauge available resources and develop ways to find savings while also addressing the needs of Spain’s people. It makes no sense that even though productivity is now higher thanks to technology, social inequality prevails.

Hopefully 2023 will see more discussion of digital identity and currencies or even universal income, and less of the words that characterised 2022: crisis, war and inflation.

Indonesia: seven-year inflation high leads to massive layoffs

Bhima Yudhistira Adhinegara, Direktur, Center of Economic and Law Studies (CELIOS)

While relatively low compared to other countries, Indonesia’s overall inflation rose to its highest level in seven years, reaching nearly 6% in September 2022. Ballooning food and subsidised fuel prices are behind this increase.

At the beginning of this year, Indonesia, the world’s biggest crude palm oil producer struggled to control cooking oil prices due to a supply bottleneck, despite enjoying the financial benefits of the commodity’s price increase.

Robby Fakhriannur/Shutterstock

More generally, the prices of staple commodities – from rice to spices – also rose on the back of failed harvests due to unpredictable weather. In addition, the ongoing war between Russia and Ukraine partially contributed to rising food prices, especially food for animals, which became more expensive and affected livestock prices. The government’s decision to raise subsidised fuel prices by 30% in September delivered a further blow to the country’s inflation rate.

This inflation has increased the cost of living as it has not been accompanied by a sufficient wage increases. In 2022, Indonesia’s minimum wage increased only by 1.09% – the lowest-ever recorded rate. With annual inflation hitting 5.51%, it means that the purchasing power for those on lower incomes has declined by 4.42%.

Job opportunities are even more limited amid high inflation rates. Export-oriented manufacturing companies have begun to carry out mass layoffs. Digital startups, the hope of young people during the pandemic, have also cut employee numbers. At the same time, four million new workers joined the labour market between August 2021 and 2022, while Indonesia already has a youth unemployment rate of 16% – relatively high for southeast Asia.

Meanwhile, to curb inflation, the central bank raised interest rates by 2% between July and December 2022, triggering an increase in lending rates. More than 70% of house purchases in Indonesia rely on mortgages and it might also now be more difficult for new businesses to access much-needed loans.

While state revenues from commodities are increasing due to the recent bonanza, inflation in 2023 is expected to remain high, mostly due to elevated transport costs driven by volatile fuel prices. The Indonesian government now needs to rethink inflation policy and public service costs such as healthcare insurance fees and public transportation rates. These items affect most people and will trigger an additional inflationary impact.

Canada: changing plans for parenthood and dating highlight cost concerns

Wayne Simpson, Professor, Department of Economics, University of Manitoba

Like almost every other country in the world, there’s been no shortage of economic uncertainty in Canada over the past year. Russia’s invasion of Ukraine disrupted global fuel supplies, causing gas prices to reach record levels. The Bank of Canada’s aggressive interest rate hikes also caused recession jitters. Inflation and the cost of living remain big concerns for Canadians in 2023.

Canadians spent less on travel over the holiday season because of these fears. And even though lower gas prices provided some relief over the same period, the price at the pumps still soared to record heights in 2022. Some experts predict they will rise again in 2023.

The price of groceries has also been a serious pain point for Canadians, and grocery costs could soar by up to 7% more in 2023. Rising food costs are in part a result of Ukraine-related disruptions in three major commodities: wheat, sunflower oil and especially fertilisers, which drove Canadian crop production costs up by 6-8% in 2022. Concerns have already been expressed about the impact of rapidly rising food prices on Canadians’ health, especially families with low incomes.

The silver lining to the economic volatility has been housing prices in Canada. Experts predict a continuing cooling trend in some of the hottest – and most unaffordable – housing markets in the country. One report forecasts the average price of a Canadian home could drop by 25% in the first quarter 2023. Prohibitively high mortgage rates, low inventory and uncertainty about where the Bank of Canada’s interest rate cycle will finally peak could explain the slowdown.

Some reports suggest Canada’s higher cost of living is even causing people to postpone parenthood. And certain dating apps report that users are keeping dates simple and economical by suggesting casual activities rather than “fancy”, expensive or elaborate nights out.

The fact that prices in other G7 countries such as the US, UK, Germany and Italy increased at an even faster rate than Canada in 2022 may be a small consolation to Canadian consumers. More sobering are forecasts of further inflation in 2023 before annual inflation settles back into the more familiar and comfortable range of 1-3% in 2024.

Alan Shipman, Senior Lecturer in Economics, The Open University; Aymen Smondel, Maître de conférences en finance, IAE de Nice, IAE Nice – Université Côte d’Azur; Bhima Yudhistira Adhinegara, Direktur, Center of Economic and Law Studies (CELIOS); John W. Diamond, Director of the Center for Public Finance at the Baker Institute, Rice University; Luis Garvía Vega, Director del Máster Universitario en Gestión de Riesgos Financieros (MUGRF) en ICADE Business School, Universidad Pontificia Comillas; Mohamad Hassan Shahrour, Maître de Conférences en Finance, Université Côte d’Azur, IAE Nice – Université Côte d’Azur; Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University, and Wayne Simpson, Professor, Department of Economics, University of Manitoba

This article was first published on The Conversation, here.

For all the latest Business News Click Here

For the latest news and updates, follow us on Google News.

Denial of responsibility! NewsBit.us is an automatic aggregator around the global media. All the content are available free on Internet. We have just arranged it in one platform for educational purpose only. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, all materials to their authors. If you are the owner of the content and do not want us to publish your materials on our website, please contact us by email – [email protected]. The content will be deleted within 24 hours.