A year ago, Deborah Mais was a passenger in a morning car wreck in College Station, Texas, that left her with a traumatic brain injury and a growing pile of seemingly insurmountable medical bills.

The out-of-pocket costs for her care now total well over $500,000. The debt has become so overwhelming, she’s stopped opening the bills when they arrive.

“My life changed that day,” said Mais, who’s since lost her home, her car and the ability to care for her three children, who are currently staying with a relative. She suffers from anxiety and depression.

“It feels unbearable sometimes,” she said.

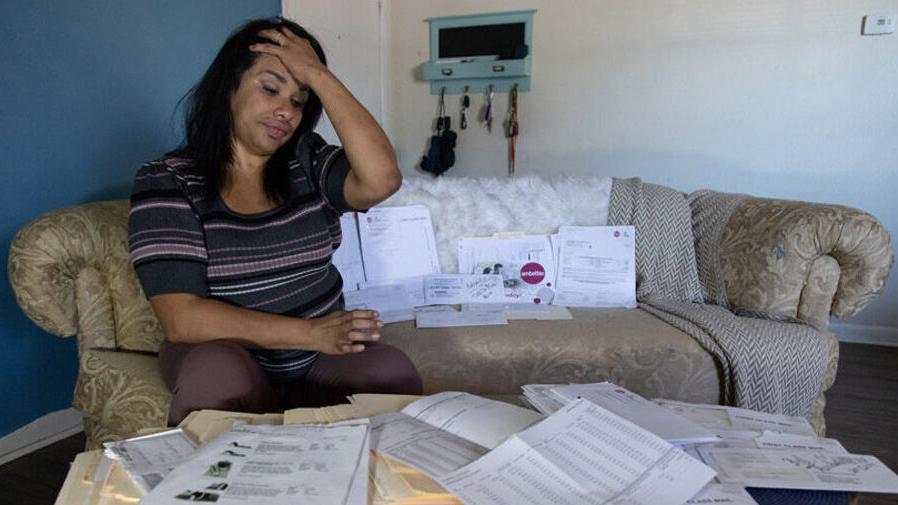

Deborah Mais sits on her mom’s couch, surrounded by her medical bills on Oct. 26 in College Station, Texas. Thirteen percent of U.S. adults have past-due medical bills.

Mais isn’t alone. One in every five people in Texas has medical debt that is in collections, one of the highest rates in the U.S.; medical debt has become a nationwide crisis, with 13% of U.S. adults impacted by past-due medical bills, according to data collected by the Urban Institute, a Washington, D.C., public policy think tank.

People are also reading…

The problem is at its worst in states where large swaths of residents are uninsured, advocates say, and as health care costs rise, the problem doesn’t appear to have an end in sight.

West Virginia, South Carolina, Oklahoma, North Carolina and Texas have the highest level of medical debt in the country. Three of those states — North Carolina, South Carolina and Texas — are home to 57 of the top 100 counties with the highest levels of medical debt, according to the data. Another 20 of those counties are in Georgia.

Experts say it’s not a coincidence that those states haven’t expanded Medicaid to provide health coverage to their lowest-income residents. Medicaid expansion is one of the key policies they believe could help tackle medical debt.

The recovery for Mais, 32, would have been an uphill climb because of the severity of her injuries alone: She spent weeks in a coma at St. Joseph Health Hospital after the Oct. 17, 2021, accident, where she was the passenger in the car determined to be at fault. She was transported by ambulance to a rehabilitation hospital in Houston three weeks later, determined to be minimally conscious at the time.

She’s now out of the hospital, but Mais still battles the lingering effects of her traumatic brain injury and faces near-constant pain from the aftermath of a fractured pelvis, ribs and tailbone that have yet to fully heal.

Medical bills for Deborah Mais sit on a living room table at her mom’s apartment in College Station, Texas. The total for these two bills is $497,569.65.

The debt has more than financial consequences. Mais’ financial struggles have disrupted her ability to heal at every step of the way, her family says. Though she had a job cleaning apartments at the time of the accident, she didn’t have health or car insurance.

“Because of the lack of proper insurance, she’s not getting proper treatment,” said Dolly Francis, Mais’ mother and primary caretaker. “From the time that she actually came out of the coma, she’s improved, but not where she really needs to be.”

Medical bills piled up over recent months, despite health insurance purchased on her behalf through the Affordable Care Act marketplace after the accident, a GoFundMe appeal and donations from a local family that helped her get admitted to the rehabilitation hospital.

Francis remembers the shock of opening a $69,000 bill, knowing there was no way the family could pay it. The bills that followed were even higher.

“I’m scared to even look,” Francis said. “People aren’t prepared for the aftermath of a situation like this, the toll it takes on everyone.”

Deborah Mais lays on her mom’s couch as Dolly Francis looks through her daughter’s medical bills at Francis’ apartment on Oct. 26 in College Station, Texas.

Where medical debt is the worst – and why

In Lenoir County, in eastern North Carolina, about 44% of adults have medical debt in collections, the highest level of any county in the U.S. The county of about 56,000 people has a rate nearly four times the national average, according to Urban Institute data, which analyzed more than 10 million records from February 2022 from a major credit bureau.

AnneMarie Comeau, who lives in Lenoir County, has a chronic condition that affects her digestive system. She is in the hospital for procedures or emergency visits several times a year. The health problems leave her unable to work.

“I have a lot of health issues,” Comeau said. “They’re not as bad as other people, but life has been painful.”

Comeau has about $5,000 in debt collections, despite qualifying for Medicare and disability insurance. At times, she elected to forgo surgeries or appointments when she had to pay for the services upfront and could not.

Researchers with the Urban Institute found that medical debt tends to be worse in certain areas of the U.S., including Southern states. Of the 100 counties in the U.S. with the highest shares of people with medical debt, 12 are in North Carolina. Texas is home to 34 of the top 100 counties. Georgia has 20 counties among the highest 100 counties, and South Carolina has 11.

All four states haven’t expanded Medicaid to provide health coverage to more lowest-income residents, a provision made available under the Affordable Care Act. More than 21 million low-income people in the 39 states that elected to expand Medicaid got coverage.

“There is clear evidence medical debt is higher in the states that have not taken up the [federal] subsidies,” said Allison Sesso, president and CEO of RIP Medical Debt, a donation-backed nonprofit group that buys medical debt from collection agencies and forgives the debt.

Sesso

Along with the lack of Medicaid expansion, there is also a correlation between race and medical debt. In almost every state, people of color tend to have higher rates of medical debt, according to the Urban Institute data.

Counties with the highest levels of medical debt have higher populations of Black residents, according to Urban Institute’s research. In the top 100 counties, nearly 24% of residents are Black, versus 12% nationally.

“There is a racial component that’s clear in the data,” Sesso said. “There are so many problems that fall on the laps of Black people. … I think the history of the United States sort of lends itself to Black people not historically having access to money, so they’re starting at a different point. We’ve never corrected from that.”

The Urban Institute’s analysis of factors that correlate to medical debt also found chronic illness was a predictor of medical debt. Residents in counties with a high number of people with medical debt are more likely to have six or more chronic conditions. The finding could play into a cyclical problem, in which people avoid medical care because of high costs, then get even sicker, Urban Institute researcher Breno Braga said.

Residents in areas with high medical debt are also nearly twice as likely to be uninsured, according to an examination of U.S. Census Bureau data and Urban Institute data.

“If you are uninsured, you’re more likely to face high out-of-pocket expenses in care,” said Urban Institute researcher Fredric Blavin. “You could potentially forgo preventive health services which, down the line, could lead to worse health outcomes and more medical debt.”

At the time of Mais’ accident, she was part of a group of 18% of Texans who lacked health insurance. Texas’ uninsured rate is double the national average.

Since the accident, she’s gone through bouts of being uninsured because of financial issues, keeping her out of inpatient rehabilitation centers that might speed up her recovery. The ACA insurance carried nearly $500 monthly premiums that were too costly to afford for long.

Rising cost of care, insurance

The rising cost of care in the U.S. is directly linked to medical debt, said Mark Rukavina, a program director for Community Catalyst, a Boston-based health advocacy organization.

Even those with health insurance aren’t immune. A Kaiser Family Foundation survey found a third of single-person households with private insurance in 2019 could not pay a $2,000 bill.

Health spending increased dramatically in recent years, according to the American Medical Association. With costs increasing, insurance becomes more expensive and employers look for ways to cut costs, Rukavina said. The most obvious solution is to push costs onto individuals, he said.

“Frankly, that’s the most reliable cost-containment strategy for an employer,” he said. “Increase their deductible. Increasing co-payments, increasing co-insurance, moving more of that cost from insurance to your worker. It’s a real problem.”

Scott Mosher, of Newton, North Carolina, discusses his ongoing struggle to pay medical bills.

Scott Mosher did just that. Mosher, who lives in the western North Carolina city of Newton, chose not to enroll in workplace insurance because of the high cost. Mosher couldn’t afford the deduction because he needed the money to get by, he said. When he started having prostate problems and pain in 2017, he didn’t seek medical care because he had no coverage.

Instead, the 53-year-old lived with the pain until it became unbearable. In 2020, after expensive emergency room trips and an unsuccessful walk-in clinic visit, he was admitted to a hospital. By then, his prostate required several surgeries and time in the hospital. Now, he has nearly $80,000 in medical debt he’s unable to pay.

“I’m working now, I found a job that pays more, but as far as all this debt — I can’t pay it.” Mosher said. “Collection companies are calling me off the rails. … My credit is hammered because of it.”

‘Top of the list’

There is no quick fix to help those with medical debt, but one policy change that is proven to decrease medical debt is Medicaid expansion, said Gabriela Elizondo-Craig, project manager of the Innovation for Justice’s Medical Debt Policy Scorecard project. The group rated states based on how policies protect consumers from medical debt and found that Medicaid expansion is at the top of the list of policy changes that could help people with medical debt, she said.

Under the ACA, states are allowed to expand Medicaid eligibility to accept people with incomes of up to 138% of the federal poverty level. Without expansion, eligibility requirements to qualify for Medicaid are more stringent.

Twelve states in the U.S. have not elected to expand Medicaid. South Dakota will soon leave that group. Voters recently approved a measure to expand Medicaid. A 2021 estimate by the Urban Institute suggests that in states that have not expanded Medicaid, about 4.4 million more people would be eligible were Medicaid expanded in all of those states.

Comeau, in North Carolina, qualified for Medicaid coverage in 2021. The coverage helped her get a necessary surgery that she previously delayed. After getting the surgery, her abdominal pain reduced significantly, she said.

“I have not felt this good in three years,” she said.

Medicaid expansion can still miss a group of people who are low-income but don’t qualify for government-subsidized coverage.

Mosher fell in that gap: unable to pay for employers’ health insurance and not qualified for Medicaid.

“I was trying to get Medicaid or something, but I couldn’t. I’m behind in everything,” Mosher said. “I was worried about getting my stuff shut down, my power and water, because I hadn’t worked for months” while hospitalized.

Scott Mosher, of Newton, North Carolina, dicusses his medical bills, which total over $80,000. (Robert C. Reed, Hickory Daily Record)

An unexpected medical bill for people like Mosher can be nearly impossible to pay, Sesso said.

It’s why RIP Medical Debt recently increased its income threshold for qualifying for debt relief from the organization, she said. In the past, someone had to make 200% of the federal poverty level to qualify. Now, it’s 400%, Sesso said.

“Because it’s those folks that don’t have another safety net protecting them,” she said.

In states where Medicaid has not been expanded to cover more people, there’s little help for those who fall between the cracks, Community Catalyst’s Rukavina said.

But it’s not just up to states to solve the problem. Rukavina said the issue can be addressed on a federal, state and hospital level.

Elizondo-Craig said one effective policy that states or hospitals can have in place is requiring screening for financial assistance. Often, people don’t know that they qualify or don’t know to ask if they are eligible, she said.

Rukavina suggests hospitals should examine their billing and charity practices.

“We need to be attacking this at all levels,” he said. “Some of this can only be addressed at the federal level, but states can do a lot and so can institutions.”

The struggle with medical debt isn’t easy, Elizondo-Craig said. The burden of unpaid medical debt can cause additional physical and mental health issues. The impact on credit scores can make it difficult for people to buy homes or get jobs.

This year, the nation’s three largest credit bureaus, Equifax, Experian and TransUnion, announced that, starting in 2023, medical debt under $500 would no longer affect consumer credit reports, according to the Consumer Financial Protection Bureau.

Starting in July of this year, medical debt must remain unpaid for at least a year before it damages one’s credit score. Previously, it took six months.

The protection can combat the effects of medical debt in the U.S., Elizondo-Craig said.

“It’s a debt they didn’t choose to incur,” Elizondo-Craig said. “It’s totally different from debt from getting consumer goods.”

Alicia Pender has incurred close to $30,000 of medical debt due to long COVID and other illnesses and injuries.

‘Like someone is looking over your shoulder’

Living under the weight of medical debt can cause stress that leads to more health problems and makes it difficult for those already struggling financially to climb out of the hole.

Debt took a toll on Alicia Pender, a travel nurse working in central North Carolina. A bout with COVID-19 in 2020 left her with a long list of health issues and more than $30,000 in medical debt, despite having insurance. She is unable to pay high deductibles and out-of-pocket costs. About half of her debt is in collections.

As the stress of her medical debt mounts, her mental health has suffered, she said.

“I can’t figure out how to get out of this hellhole, this quicksand,” she said. “It’s a vicious cycle that having poor physical health has led me to having poor mental health. It just feels like everything is adding up, and the more it adds up, the more the frustration and depression mounts up, and there’s no end in sight.”

Collection agencies call daily, Pender said. With constant calls and collection letters, people with unpaid medical debt are always worried about it, RIP Medical Debt’s Sesso said.

“You feel like someone is looking over your shoulder and that feels very overwhelming to people,” Sesso said. “People feel like they’re failures – like they’ve done something wrong and they failed, and it’s not that. It’s the system.”

People want to pay their debt, but medical debt is more likely to affect those with low incomes, she said. In the top 100 counties where medical debt is the highest, families have an average household income of $57,825 annually, compared to the national average of $88,607, according to the Urban Institute’s analysis.

Comeau, the Lenoir County resident, sometimes found herself canceling phone service or other secondary needs to stay afloat as medical bills accumulated.

“I’m not worried about the medical bills,” she said. “I’m more concerned about food for my family and my medication. It is what it is. There are too many other things to worry about.”

For Mais, in Texas, there hasn’t been much time to think about the piling bills. Healing is still a full-time job. She said she envisions a future where she can live independently and raise her sons.

“I think God gave me another chance for a reason, and I’m here,” she said. “So there has to be a good ending to this story.”

Deborah Mais gets emotional during an interview on Oct. 26.

Mais’ brother, Brian Thornton, worries about the financial devastation of the situation continuing to impact her long after any physical wounds heal.

“If she were to ever become independent again, that is going to be something she’ll have to deal with,” Thornton said. “It’s going to be tragic. It would be a huge accomplishment to heal to that point.

“If and when she does, she’ll find herself in a bind in terms of finances and outstanding bills.”

PHOTOS: Dealing with medical debt

Deborah Mais feeds her mom’s fish at her apartment on Wednesday, Oct. 26, in College Station, Texas.

Deborah Mais works on doing the dishes at her mom’s apartment on Oct. 26 in College Station, Texas.

Deborah Mais works in her mom’s kitchen at her apartment on Wednesday, Oct. 26, in College Station, Texas.

Deborah Mais lays on her mom’s couch as Dolly Francis looks through her daughter’s medical bills at Francis’ apartment on Wednesday, Oct. 26, in College Station, Texas.

Dolly Francis, left, and her daughter Deborah Mais hold one of Mais’ medical bills at Francis’ apartment on Oct. 26 in College Station, Texas.

Dolly Francis, left, and her daughter Deborah Mais pose in front of stacks of medical bills at Francis’ apartment on Oct. 26 in College Station, Texas.

Dolly Francis, left, and her daughter Deborah Mais pose in front of stacks of medical bills Francis’ apartment on Oct. 26 in College Station, Texas.

Deborah Mais poses with a stack of medical bills at her mom’s apartment on Wednesday, Oct. 26, in College Station, Texas.

An envelope containing a medical bill addressed to Deborah Mais for $336,850 sits on a living room table at her mom’s apartment on Wednesday, Oct. 26, in College Station, Texas.

Deborah Mais admires a gift her middle son, Logan, gave her for Mother’s Day at her mom’s kitchen table in her apartment on Wednesday, Oct. 26 in College Station, Texas.

Medical bills for Deborah Mais sit on a living room table at her mom’s apartment in College Station, Texas. The total for these two bills is $497,569.65.

Dolly Francis, left, and her daughter Deborah Mais pose in front of stacks of medical bills at Francis’ apartment on Oct. 26 in College Station, Texas.

Deborah Mais holds an envelope containing a medical bill for $138,743.25 at her mom’s apartment on Wednesday, Oct. 26, in College Station, Texas.

Dolly Francis has been using manila envelopes to keep each of her daughter’s medical bills separated and organized.

A view of an itemized bill for Deborah Mais is shown at her mom’s apartment on Oct. 26 in College Station, Texas.

Deborah Mais poses with a gift her middle son, Logan, gave her for Mother’s Day at her mom’s kitchen table in her apartment on Oct. 26 in College Station, Texas.

Deborah Mais gets emotional during an interview on Oct. 26.

Deborah Mais listens in her mom’s apartment on Oct. 26 in College Station, Texas, as her mother talks about an auto accident and Mais’ three boys.

Deborah Mais sits on her mom’s couch, surrounded by her medical bills on Oct. 26 in College Station, Texas. Thirteen percent of U.S. adults have past-due medical bills.

Deborah Mais lays on her mom’s couch as Dolly Francis looks through her daughter’s medical bills at Francis’ apartment on Oct. 26 in College Station, Texas.

Scott Mosher, of Newton, North Carolina, talks about his medical bills, which now total nearly $80,000.

Scott Mosher, of Newton, North Carolina, discusses his ongoing struggle to pay medical bills.

Alicia Pender has incurred close to $30,000 of medical debt due to long COVID and other illnesses and injuries.

For all the latest Health News Click Here

For the latest news and updates, follow us on Google News.

Denial of responsibility! NewsBit.us is an automatic aggregator around the global media. All the content are available free on Internet. We have just arranged it in one platform for educational purpose only. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, all materials to their authors. If you are the owner of the content and do not want us to publish your materials on our website, please contact us by email – [email protected]. The content will be deleted within 24 hours.